How Credit Score Works is something most people only start understanding after their loan application suddenly gets rejected. Your phone buzzes daily with SMS spam offering “Pre-Approved Personal Loans!” and lifetime-free credit cards. But the moment you actually apply for a home loan or need emergency funds, the bank system auto-rejects your file because of a tiny three-digit number.

A massive chunk of the population only starts caring about their credit score exactly five minutes after their loan application bounces. By then, the damage is already done.

Let’s strip away the banking jargon. Your credit score isn’t some random luck-based number generated by a bank manager. It is a highly calculated mathematical reflection of your financial discipline.

A massive chunk of the population only starts caring about their credit score exactly five minutes after their loan application bounces. By then, the damage is already done.

Let’s strip away the banking jargon. Your credit score isn’t some random luck-based number generated by a bank manager. It is a highly calculated mathematical reflection of your financial discipline. This guide by Jobcareermint.com breaks down exactly what is happening behind the scenes, how the algorithm judges you, and what you actually need to do to fix a broken credit profile this year.

What Actually Is a Credit Score?

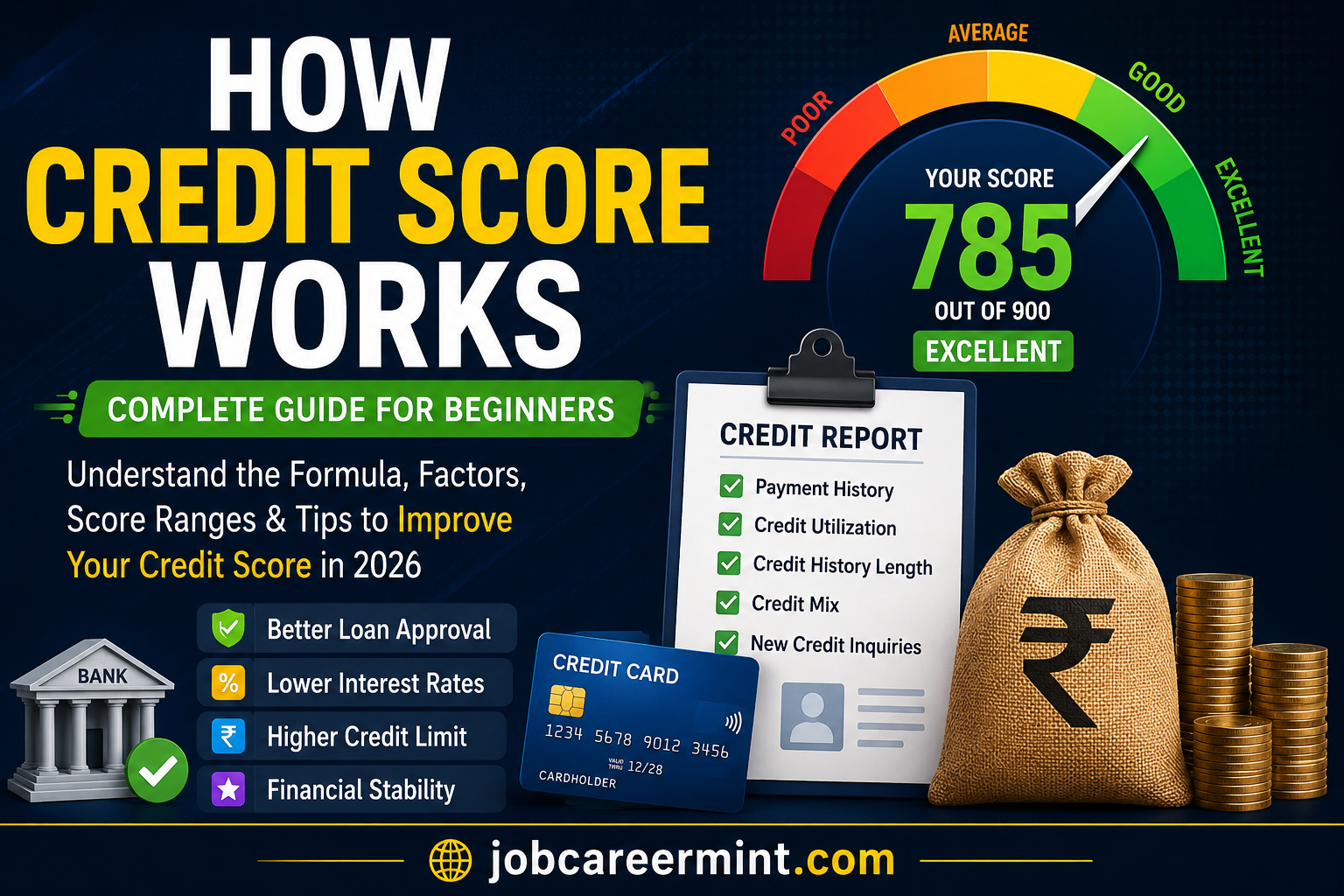

Think of it as your financial report card for adulthood. It ranges from 300 to 900.

When you walk into a bank asking for money, the lender has zero idea if you are a responsible borrower or a serial defaulter. Instead of guessing, they pull your credit file. If you are sitting above 750, they roll out the red carpet with low interest rates. If you are lingering in the 500s, you will struggle to finance a basic smartphone on EMI.

Credit Score vs. CIBIL Score: Stop Mixing Them Up

This is the ultimate rookie mistake. People use the terms “CIBIL” and “Credit Score” like they mean the exact same thing. They don’t.

Credit score is the general concept. CIBIL is just a private company (TransUnion CIBIL) that happens to calculate it. India currently operates with four major licensed credit bureaus:

- TransUnion CIBIL (The most popular one)

- Experian

- Equifax

- CRIF High Mark

Different banks pull reports from different bureaus. That is exactly why your score might show up as 760 on one app and 745 on another.

The Surveillance: How the Backend Works

Your bank is not sitting in a room judging your character. The system is completely automated.

Understanding how credit score works can completely change your financial future because banks use this score to decide your loan approval chances, credit card eligibility, and even interest rates.

Every single month, your bank, your credit card issuer, and even that Buy-Now-Pay-Later app you used for ordering shoes send a massive data dump to the credit bureaus. They report if you paid your EMI on the 5th or the 15th. They report how much of your card limit you exhausted. The bureau’s algorithm crunches that raw data and updates your score. You are constantly being graded.

The 5 Core Pillars Controlling Your Score

The exact algorithm is a corporate secret, but the weightage is public knowledge. If you want to hack your score, focus purely on these five areas.

1. Payment History (The Dealbreaker)

This is the absolute core of your profile. One bounced EMI cheque or a credit card bill paid 10 days late can tank your score by 40 points instantly. Lenders forgive a lot of things, but they do not forgive missed payments. That black mark stays on your digital record for up to three years.

2. Credit Utilisation Ratio (CUR)

This shows how desperate you are for credit. If your card has a ₹1,00,000 limit and you spend ₹90,000 every month, you look cash-starved to the algorithm. Keep your total utilization strictly under 30%. If you need to spend more, ask your bank for a limit enhancement to balance the ratio.

3. Age of Credit History

Banks love old, boring, predictable data. If you have a credit card from five years ago that you pay off cleanly every month, keep it active. Closing your oldest credit account wipes out years of good history and immediately shortens your credit age.

4. Credit Mix

Having just five different credit cards doesn’t make you look good. A healthy profile has a mix of unsecured loans (credit cards, personal loans) and secured loans (auto loans, home loans). It proves you can handle different types of financial pressure.

5. Hard Inquiries

Stop downloading random loan apps just to “check your eligibility.” Every time you hit apply, the lender pulls your official file from the bureau. This is called a hard inquiry. Five hard inquiries in a single month signals to the algorithm that you are desperately hunting for cash.

Decoding the Indian Credit Score Ranges

| The Score Range | What It Means | The Reality at the Bank |

|---|---|---|

| 750 – 900 | Excellent | Instant approvals, negotiation power on interest rates. |

| 700 – 749 | Good | Loans approved, but you accept the bank’s standard terms. |

| 650 – 699 | Average | Heavy questioning. High interest rates applied. |

| 300 – 649 | Poor to Very Poor | Immediate auto-rejection by major banks. |

The “No History” Trap (NH/NA)

Never taken a loan? Never owned a credit card? You might think your financial slate is squeaky clean.

The problem is, to the banking algorithm, you are a ghost. You will likely get an “NH” (No History) or “-1” rating. Lenders cannot approve a massive home loan for someone who hasn’t proven they can handle a basic ₹10,000 credit limit first. You have to build a profile from scratch.

The Minimum Due Trap Destroying Your Score

Your credit card statement shows a “Total Due” and a much smaller “Minimum Amount Due.” Paying just the minimum is a massive psychological trap. Yes, paying it stops the bank from legally declaring you a defaulter. However, the remaining balance rolls over, incurs heavy 36% to 42% annual interest, and permanently maxes out your credit utilization ratio. Your score will slowly bleed out month by month.

Quick Fire FAQs

Does checking my own score hurt it?

No. When you check your own score on apps like GPay or Cred, it registers as a “Soft Inquiry.” It has absolutely zero impact on your numbers.

Can I pay someone to fix my CIBIL?

Absolutely not. Any agency claiming they can hack the bureau or illegally wipe out your defaults in exchange for cash is running a scam. The only way out is paying off the debt and letting time heal the profile.

Final Thoughts: Your Digital Reputation

Your credit score is no longer just a boring banking metric. It dictates your financial leverage. A jump from a 680 to a 780 can literally save you lakhs of rupees in interest payments over a 20-year home loan. Treat this three-digit number like an asset. Pay your bills three days early, don’t max out your plastic, and stop applying for loans you don’t actually need.

For more blunt financial truths, credit repair strategies, and modern career growth blueprints, keep your eyes on the updates at Jobcareermint.com.

Education & Career News Writer at JobCareerMint. Covers latest government jobs, board results, admit cards, recruitment updates and education news across India.